What is a premium in health insurance? If you’ve ever wondered about the term “premium” in health insurance, you’ve come to the right place! In this article, we’ll break down what a premium is and why it’s an important aspect of your health insurance coverage. So, let’s dive in and uncover the ins and outs of health insurance premiums!

When it comes to health insurance, a premium is the amount of money that you pay on a regular basis to maintain your coverage. Think of it as a membership fee or a subscription cost for your health insurance plan. Just like Netflix or a gym membership, you pay a premium to ensure that your health insurance is active and ready to provide coverage when you need it.

The premium you pay can vary depending on several factors, such as your age, location, and the level of coverage you choose. It’s important to understand that a higher premium doesn’t necessarily mean better coverage. You want to find a balance between a premium that fits your budget and a plan that meets your healthcare needs. Now that you know what a premium is, let’s explore how it impacts your health insurance coverage!

Understanding Premiums in Health Insurance: A Comprehensive Guide

Welcome to our guide on understanding premiums in health insurance. In this article, we will delve into the intricacies of health insurance premiums, their significance, and how they affect your coverage. Whether you’re new to the world of health insurance or looking to gain a deeper understanding, this guide will provide you with valuable insights. Let’s begin!

What is a Premium in Health Insurance?

A premium in health insurance refers to the cost you pay regularly to maintain your health insurance coverage. It’s typically a monthly payment made to your insurance provider to keep your policy active. The premium amount can vary based on a range of factors, including your age, location, coverage type, and the insurance provider.

Premiums serve as a source of revenue for insurance companies, enabling them to cover the costs of healthcare services, administrative expenses, and profits. It’s important to understand your premium and its impact on your overall healthcare expenses.

Now that we have a basic understanding of what a premium is in health insurance, let’s explore its different aspects in more detail.

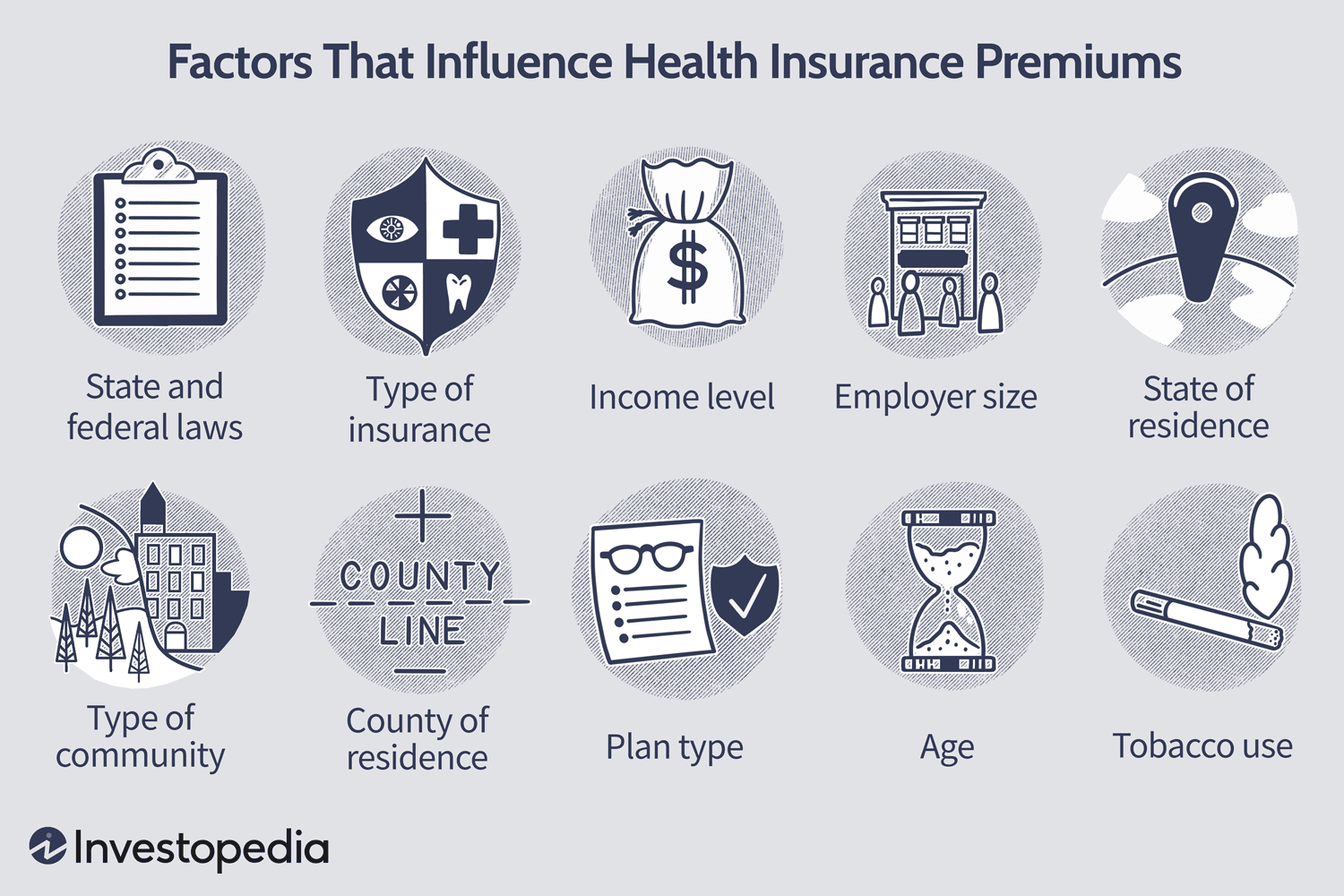

Factors Influencing Health Insurance Premiums

Several factors can influence how health insurance premiums are calculated. These factors can vary depending on the insurance provider and the specific policy. Here are some common factors that influence health insurance premiums:

- Age: Younger individuals tend to have lower premiums, as they are generally considered healthier and at lower risk of requiring frequent medical care.

- Location: Premiums can also vary based on the location where you live. Areas with a higher cost of living or where healthcare services are more expensive may have higher premiums.

- Health history and pre-existing conditions: Individuals with pre-existing conditions or a history of medical issues may have higher premiums, as they are seen as higher risk by insurance providers.

- Coverage type and level: The extent of coverage you choose, such as a basic plan or a comprehensive plan, will affect your premium. Plans with higher coverage levels typically have higher premiums.

- Smoking and tobacco use: Tobacco users are generally charged higher premiums due to the associated health risks.

These are just a few examples of the factors that can influence health insurance premiums. It’s important to consider these factors when selecting a health insurance plan that suits your needs and budget.

Types of Health Insurance Premiums

Health insurance premiums can be categorized into different types, depending on the structure of the payment. Let’s take a closer look at the types of health insurance premiums you may come across:

- Individual Premiums: This type of premium applies to individual health insurance policies, where the coverage is for a single individual.

- Family Premiums: Family premiums cover the entire family under a single health insurance policy. These premiums can typically cover the policyholder, spouse, and dependents.

- Employer-Sponsored Premiums: Many individuals receive health insurance coverage through their employers. In such cases, the premiums are partially or fully paid by the employer.

- Group Premiums: Group premiums are offered to members of a specific organization or association, such as employees of a company or members of a professional association.

- Catastrophic Premiums: Catastrophic premiums are designed for high-deductible health plans that provide coverage for major healthcare expenses after a certain deductible amount is met. These premiums are typically lower but come with higher out-of-pocket costs.

Understanding the different types of health insurance premiums can help you make informed decisions when selecting a policy.

Ways to Manage and Reduce Health Insurance Premiums

Paying health insurance premiums can sometimes put a strain on your finances. However, there are strategies you can employ to manage and even reduce your health insurance premiums. Here are some tips:

- Shop around: Don’t settle for the first health insurance policy you come across. Compare different plans from multiple providers to find the best premium rates for the coverage you need.

- Increase deductible: Opting for a higher deductible can help lower your premium. However, make sure you have enough savings to cover the deductible if needed.

- Stay healthy: Maintaining a healthy lifestyle can not only improve your well-being but also result in lower premiums. Many insurance providers offer incentives or discounts for policyholders who lead healthy lifestyles.

- Consider different coverage options: Assess your healthcare needs and determine if you can opt for a different coverage level, as higher coverage plans usually have higher premiums.

- Look for subsidies: Depending on your income and eligibility, you may qualify for government subsidies that can help reduce your health insurance premiums.

By implementing these strategies, you can effectively manage your health insurance premiums and ensure that you have the coverage you need at an affordable cost.

Conclusion

In this comprehensive guide, we have discussed what premiums are in health insurance and their significance in maintaining your coverage. We’ve explored the factors that influence premiums, different types of premiums, and provided tips on managing and reducing your premium costs. By understanding premiums and making informed choices, you can select a health insurance policy that aligns with your needs and budget. Remember to regularly review your coverage and reassess your premium options to ensure you have the most suitable policy for your healthcare needs.

Key Takeaways

- A premium in health insurance is the amount paid by an individual to an insurance company on a regular basis

- It is like a membership fee to stay enrolled in the insurance plan and receive benefits

- The premium amount can vary based on factors like age, location, health condition, and the type of coverage chosen

- Paying a higher premium usually means more comprehensive coverage and lower out-of-pocket expenses

- It is important to pay premiums on time to avoid losing coverage and to ensure continuous protection

Frequently Asked Questions

Health insurance can be complex, and understanding the various terms and concepts can be overwhelming. One important aspect of health insurance is the premium. Here are some common questions about what a premium in health insurance is and its significance.

1. Why do I have to pay a premium for my health insurance?

Paying a premium for your health insurance is essential because it helps cover the cost of your healthcare coverage. Think of it as a monthly fee you pay to be able to access medical services whenever you need them. The premium you pay contributes to the overall pool of funds that the insurance company uses to pay for healthcare services and claims.

Without a premium, insurance companies would not have the necessary funds to provide coverage for medical expenses when you require them. The premium also helps ensure that the insurer can continue to provide coverage to all policyholders, including those with higher healthcare costs. So, paying a premium is crucial to securing the financial protection and access to medical care that health insurance offers.

2. How is the premium amount determined for health insurance?

The premium amount for health insurance is determined by various factors, including your age, location, type of coverage, and the insurance company’s pricing structure. Insurance companies assess the risk associated with insuring you based on these factors. For example, younger individuals may have lower premiums because they typically have fewer health issues, while older individuals may have higher premiums due to an increased risk of medical conditions.

The location factor considers the cost of healthcare services in your area. If you live in an area with higher healthcare costs, your premium may be higher. Additionally, the type of coverage you choose and the level of benefits it offers can impact your premium amount. Insurance companies also consider their own costs, administrative expenses, and desired profit margins when setting premium rates. Therefore, various factors are taken into account to determine your health insurance premium.

3. Can my health insurance premium increase over time?

Yes, it is possible for health insurance premiums to increase over time. Insurance companies may adjust their premium rates annually based on various factors, including the overall cost of healthcare, inflation, changes in healthcare policy, and the age composition of policyholders. As healthcare costs rise, insurance companies may need to increase premiums to sustain coverage and meet the financial demands of providing healthcare services.

However, it’s important to note that any premium increases must adhere to regulations set by state insurance departments. These regulations aim to protect consumers from arbitrary and excessive rate increases. Insurance companies are typically required to justify any proposed premium increases to the regulatory authorities.

4. Can I lower my health insurance premium?

Yes, there are certain strategies that may help you lower your health insurance premium. One option is to consider a plan with a higher deductible, which means you’ll have to pay more out-of-pocket before the insurance coverage kicks in. Higher deductible plans often have lower premiums. However, it’s essential to evaluate your healthcare needs and financial situation to determine if a higher deductible plan is suitable for you.

Another way to potentially lower your premium is to compare health insurance plans and shop around for the best rates. Insurance companies may offer different premiums for similar coverage, so it’s worth exploring your options. Additionally, some employers may offer health insurance plans with lower premiums as part of their employee benefits package. Taking advantage of such opportunities can help reduce your health insurance costs.

5. What happens if I don’t pay my health insurance premium?

If you don’t pay your health insurance premium, your coverage may be at risk. Insurance companies generally have grace periods for premium payment, but if you fail to make the payment within the specified grace period, your coverage can be terminated. Losing health insurance coverage can leave you financially vulnerable in case of unexpected medical expenses.

If you find yourself unable to pay your premium, it’s essential to contact your insurance company immediately. They may be able to provide you with options, such as a temporary suspension of premium payment or enrollment in a different plan with a lower premium. It’s better to explore these options to maintain your coverage and ensure you have access to healthcare services when needed.

Understanding Health Insurance: Premiums

Summary

Health insurance premiums are the amount of money you pay every month to keep your insurance coverage. Premiums help insurance companies to pay for the medical expenses of the people they insure. Premiums can vary based on different factors like your age, the type of coverage you choose, and where you live.

In this article, we learned that health insurance premiums are important because they ensure that you have financial protection when you need medical care. Without premiums, it would be hard to afford the cost of healthcare. Premiums also help to balance out the risk for insurance companies, so they can provide coverage to everyone who needs it.

Remember, when choosing a health insurance plan, it’s important to understand how premiums work and how much you can afford to pay. Reading the fine print, comparing different plans, and talking to an insurance expert can help you make the best decision for your needs. By understanding premiums, you can take control of your healthcare and make informed choices that protect your health and your wallet.